Spousal Transfers

One tax strategy that often comes up when we work with dual-nationality couples wherein one spouse is a US person and the other is not, is the “spousal transfer.” This involves transferring low-cost basis, appreciated stock from the US spouse to the non-US spouse. In this circumstance, there is great opportunity for US capital gains tax savings, particularly in Singapore where there is no capital gains tax for residents.

What are the rules?

In any given year, an American married to a non-American has an IRS imposed limit on the amount that can be transferred to the non-US spouse without US tax implications. In 2026, this sum is USD $194,000. Every year or so, the level increases with inflation (e.g., in 2027, it might be USD $200,000).

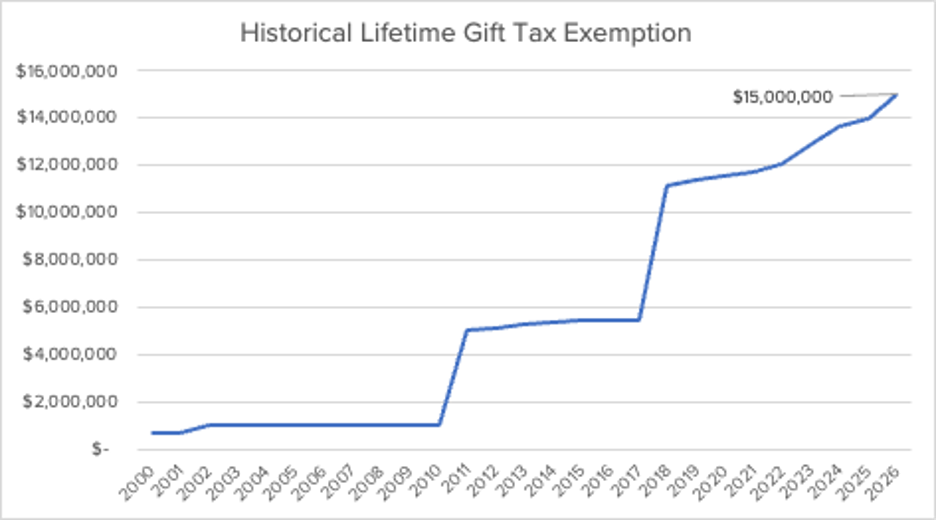

It is possible to transfer more than the IRS limit. However, the amount in excess of the threshold will be considered a reportable gift on Form 709 that counts against your lifetime unified gift and estate tax exemption. In 2026, this exemption is USD $15MM, so there is a pretty wide berth for gifting without owing tax. Saying that, this limit ebbs and flows over time, and it can be higher or lower in the future. Per the below chart, it is historically high. Once gifts/bequests exceed the USD $15MM mark, there can be taxed owed up to 40% of the fair market value (FMV).

Why would you transfer stock?

Let’s say that John is a US citizen and has worked at Google for the last 10 years. His wife, Yoko, is Japanese. They both live in Singapore. He has employer stock that has appreciated significantly. Some of it, from when he first started working, has a cost basis of USD $50k. The current FMV of this stock is USD $170k, so there are USD $120k of gains. John could transfer the USD $170k to Yoko without incurring any US tax implications. Assuming he is at the highest US long-term capital gains tax rate of 23.8%, if he were to sell that appreciated stock, there would be tax owed of USD ~$28.5k. However, once he transfers the position to Yoko, if she were to sell it, there would be USD $0 of tax owed. In other words, John can save USD ~$28.5k annually by implementing a gifting strategy. Not bad, John, and thank you, Yoko!

Why wouldn’t you transfer stock?

The main reason is that once the stock is transferred, it is no longer yours. It is a completed gift, and you no longer have ownership over the asset. This might work for some people; for others, it may not.

Additionally, it is not beneficial for non-US persons to own US situs assets, including US stock for estate tax purposes. So, in this regard, Yoko may not want to hold this much US stock long-term.

Conclusion

As a US person living abroad with a non-US spouse, there are certain benefits that can pertain to you from a cultural to a tax-financial standpoint. This can lead to impactful financial savings-growth over the long term. However, there is not a one-size-fits-all solution. Each strategy must be examined and personalized based on your circumstances, time horizon, and values, among other factors. What works great for one individual/family may not be advisable for another.

For more information on how spousal gifting strategies could be of benefit to you, please reach out to one of our wealth planners.

This material is intended for educational and informational purposes only. It is not intended to provide specific advice or recommendations for any individual. Additionally, you should consult with your Financial Advisor, Tax Advisor, or Attorney on your specific situation. The views expressed in the material are that of the author and do not necessarily reflect those of any market, regulatory body, State or Federal Agency, or Association. All efforts have been made to report or share true and accurate information. However, the information may become materially outdated or otherwise rendered incorrect due to subsequent new research or other changes, without notice. The author nor the firm are able to always verify the content from third-party sources. For additional information about the firm, please visit the MAS Website at https://www.mas.gov.sg/ and the SEC Website at www.adviserinfo.sec.gov. For a copy of the firm's ADV Part 2 Brochure, please contact us at info@avriowealth.com.