Retirement: Bond Ladders

Do Bond Ladders Have a Place in Retirement Portfolios during Your Drawdown Years?

With the focus shifting to enjoying retirement, a reliable income is paramount. Ensuring the safety of the initial sum is important, as market corrections and bear markets are inevitable. Removing the anxiety caused by market volatility can be very important to long-term outcomes and good decision-making when relying on a portfolio for living expenses.

A well-diversified portfolio of high-quality stocks and bonds has been the typical advice, often accompanied by a list of eight to ten basic rules for investing after retirement:

- Budget your expenses accurately

- Aim for tax efficiency

- Hold sufficient cash reserves

- Be diversified but keep sufficient long-term stocks to mitigate inflation risks

- Mitigate sequence-of-returns risk

- Do not make decisions based on emotions, especially fear

- Take professional advice

- Manage your estate planning

- Enjoy life

Retirees are finding 2022 to be an emotional challenge. Since the mid-1970s, the worst year for most bond indexes was 1994 when the US Central Bank hiked the key short-term interest rate six times and 2.5% in total. That left indexes with typically 2.9% losses on the year. For 2022 year to date, most bond indexes are bearing losses of 8–10% or greater, when many stock indexes are in bear market territory. At the same time, the globe is experiencing the first serious cost of living spike since the 1970s!

Whilst this is disconcerting, there are proven investment tactics that are designed to take care of a situation like this, and investors should not despair. The long-term bond bull market has led to considerable marketing success for many fund managers’ “bond fund” products, with much focus on diversification and the idea of “safe.” Redeeming moneys from most bond funds requires selling units of the fund to a buyer at the price they are willing to pay. Sometimes market sentiment makes the prevailing price unattractive. Individual bonds afford the owner the option to hold until maturity and receive the capital repayment no matter the bond market sentiment.

Over the long run, the total return of bonds depends far more on their income than on changes in price. Since 1976, just over 90% of the average annual return of the U.S. bond market has come from interest and reinvesting it. Most bond funds are, in effect, perpetual in nature; they are designed for the long term.

If you are in your retirement years, your passive income from rentals, interest, and dividends will likely be part of your living needs. It is highly likely that, on average, there will be a need to liquidate some assets to meet the cashflow requirement or risk running down cash reserves for a period to avoid selling assets at lower prices.

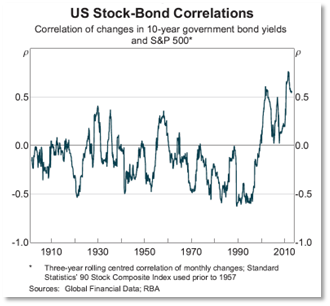

At the crux of typical planning advice and the basis for the construction of diversified investment portfolios is the assumption of imperfect correlation of asset returns (Markowitz 1952, Sharpe 1964). That may have been a reasonable assumption over the course of the 20th century (although not always), but so far this is not the case in the 21st century. The correlation has been weakly positive (see below).

The assumption of imperfect correlation (or indeed negative correlation) has led to the proliferation of the use of bond funds with a constant duration as a relatively “safe” asset that reduces portfolio riskiness. That has worked well while both nominal and real yields have been falling, but it could be problematic when yields are rising (bond prices are falling) or remain volatile.

Sources: Vanguard calculations (data 1935- 31 December 2021)

The above table points to the “next five years” as the “risky timeframe” if it is stocks that are being switched to lower risk. It also strongly suggests that cash is not a prudent choice for investment.

Most manage sequencing risk (where low asset prices make it unattractive to sell assets in some years) by creating a “bucket” of investments parked in low-risk assets to provide certainty that several years of the needed income will be available even in times when selling risky assets could harm long-term performance. Once conditions improve, topping up of the low-risk bucket resumes.

The reality of using a typical, short-duration bond fund as one of the lower-risk stores of wealth has been exposed in 2022. Many have lost some 7–9% of their capital value in the first eight months of 2022. Even the perceived risk-free Bloomberg 1–5 Yr Treasury USD has decreased in value by some 4.7% year to date. Like stocks, bonds owned via bond funds are now a source of angst for many investors.

However, there’s an effective way to ease this angst. It’s called a bond ladder—a strategy that involves buying individual bonds of varying, sequential maturities. Then holding these bonds until maturity. Not only does this provide a certain cash flow, but you also get to take advantage of higher rates without the risk of capital loss.

Source: https://seekingalpha.com/article/4281609-bond-ladder-can-protect-destroy-your-portfolio

In most times, the available yield to maturity of the next batch of 5-year bonds on offer to be purchased to replace the cash taken from year zero are higher than those of years 1,2,3, and 4.

The two risks that often get mentioned with regard to this strategy:

- Reinvestment Risk—when replacing money withdrawn from the portfolio, the new 5-year bond has a lower yield to maturity than what is being replaced

- Credit Risk—most portfolios can only own a few individual bonds because of the minimum nominal value that can be purchased. Therefore, at first glance the concentration of the risk of default can concern some observers.

Mitigation of these risks is unnecessary when the individual bond ownership is thought through from the perspective of the entire investment portfolio.

Reinvestment risk is mitigated by the fact that in any given year, unless the pricing is exceptionally attractive, you are only adding one year’s sequential yield to the portfolio. Nobody can accurately predict whether next year the available yield to maturity or, indeed, yield adjusted for inflation will be higher or lower than the present. You are spreading reinvestment risk over time.

The risk of the default needs to be thought of in terms of all of the capital drawdown from a portfolio coming from a single security; typically the maturing bond redemption funds will account for 12–30% of the cash flow. If the portfolio drawdown were 5% per annum, then the loss default risk would account for 0.6%–1.5% of the overall portfolio value. Could your retirement strategy withstand such a loss? Probably yes.

Holding bonds until maturity reduces interest rate risk, as this enables investors to avoid selling on the secondary market, which may be pricing your bonds at a loss at the time you might decide to sell them.

Constructing and managing a productive cashflow matching bond ladder is more complex than it appears. It requires extensive knowledge of the dynamics and nuances of the bond market.

Here are a few points to keep in mind:

- The first rule of a bond ladder is to have discipline—to avoid selling a bond at a loss. Usually, the simplest way to avert this is to plan long in advance to hold bonds until maturity.

- Many investors focus on yield alone, but this is a simplistic approach that can be extremely faulty. The focus needs to be on matching future cash flow needs. The yield achieved from the individual bond is typically a very small portion of future income. Being confident that the bond issuer will repay the capital is more important. Select bonds based on the credit quality of the issuer: stay with very high quality and let your remaining growth portfolio take care of long-term inflation.

- Effective ladders can be built from various types of bonds, depending on an investor’s tax situation. Understanding your tax efficiency can substantially impact the cash flow.

- US investors have the option to use Defined Maturity Bond ETFs to build ladders as well as individual bonds. Such products are designed for US investors and typically do not suit foreign investors.

By working with an advisor and possibly a bond manager, you can structure a bond ladder that makes sense for your overall asset allocation, long-term goals, and risk tolerance. Creating an individual bond portfolio can help you position for income and wealth preservation. During this difficult market period, these benefits can ease angst considerably.

This material is intended for educational and informational purposes only. It is not intended to provide specific advice or recommendations for any individual. Additionally, you should consult with your Financial Advisor, Tax Advisor, or Attorney on your specific situation. The views expressed in the material are that of the author and do not necessarily reflect those of any market, regulatory body, State or Federal Agency, or Association. All efforts have been made to report or share true and accurate information. However, the information may become materially outdated or otherwise rendered incorrect due to subsequent new research or other changes, without notice. The author nor the firm are able to always verify the content from third-party sources. For additional information about the firm, please visit the MAS Website at https://www.mas.gov.sg/ and the SEC Website at www.adviserinfo.sec.gov. For a copy of the firm's ADV Part 2 Brochure, please contact us at info@avriowealth.com.