Currency Risk

Currency risk is the potential for financial loss due to changes in exchange rates between two or more currencies. Foreign exchange (FX) movements arise due to numerous factors such as interest rates, trade deficits, economic conditions, political instability, or market conditions. To some degree, currency risk is embedded in the portfolios of every international investor. So it’s surprising that such an important topic is often ignored, mismanaged, or misunderstood from both outside and inside the financial planning community. Recent geopolitical conflict has resulted in significant currency movements across various currency pairs. With increased volatility and the dollar rising, it may be a good time to quickly review currency risk and understand how currency exposure in your personal investment portfolio aligns with your objectives.

Currency Risk

Currency risk exists when your assets or an income are valued in a different currency to your future liabilities. From the point of view of a typical investor, currency risk occurs when the currency of an investment varies against the reference currency. The reference currency is that of your future liabilities—examples include the currency of the country where you live, plan to retire, or the currency you need to pay university fees in.

Most people who live and work internationally have experienced the impact of positive or negative currency movements. When I first arrived in Singapore in 2007, the exchange rate between the Singapore dollar the British pound was 3:1. Then, over in Thailand, British pensioners could afford to live off a government pension; where one British pound converted to over 70 Thai Baht. Over the years, many Thai communities popular with expats such Hua Hin suffered as the rates changed. Indeed the property market suffered heavily as the pound weakened, leaving many Brits with no option but to return home; an unfortunate testament to the appreciating Thai Baht.

Of course currency movements can impact our lives in a multitude of ways. Perhaps you’re sending money home, paying a mortgage in a different currency, or receiving monies from a tenant overseas. Payments can be greater or lesser than before because you get paid in a stronger or weaker currency. Or maybe your child wants to attend university in a country whose currency has depreciated against that of your savings, so it’s now less expensive.

Appreciating Singapore Dollar

In Southeast Asia, we have experienced some dramatic currency fluctuations in recent times. Predicting long-term trends is far from an exact science. Some currencies provide for more stability than others. We often need to blend our desire to protect against currency risk with the need to effectively asset allocate and benefit from exposure to US equity markets.

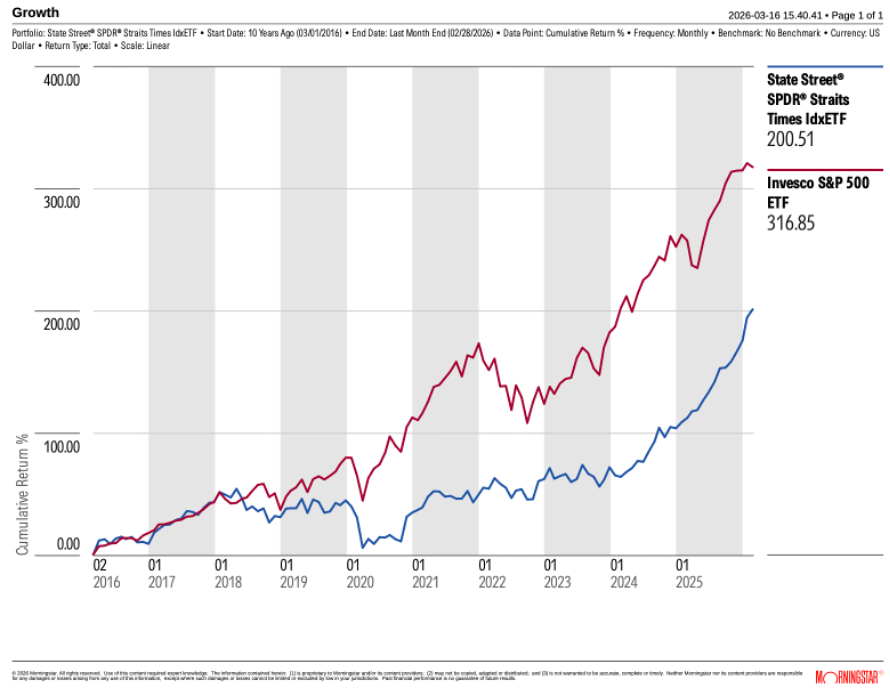

For example if an investor believed the Singapore dollar would appreciate over the last 10 years and so invested in the Straits Times Index (STI) via a SGD Exchange Traded Fund (ETF), they would have benefited from a cumulative total return of 200.51%. However, if they invested in the same Index using US dollars, they would have received a cumulative total return of 170.23%. The difference can be explained as the USD/SGD moved from S$1.37 to S$1.28 representing a depreciating dollar to the tune of 6.6% over the SGD over the decade.

However, the tech-heavy S&P500, which grew from approximately 2,022 points in March 2016 to 6,740 points in March 2026, would have given a cumulative total return of 316.85%. Thus, it’s fair to say the Straits Times Index has lagged behind. Even taking into account the change in FX rates, one would still have been better off invested in the S&P 500 during the period.

Currency Risk Derives From The Valuation Currency Of The Base Asset

If your asset is in the same currency as your reference currency then you don’t have currency risk. But if the asset is valued in a different currency, you have that risk. For example, an investor based in Singapore, whose home currency is Singapore dollars will be exposed to currency risk by owning a property in the UK. If the market value of the property rises by 10%, and sterling falls 10% then the net growth is zero. The larger risk is holding a loan in an alternate currency where the rates move against, thereby creating a liability mismatch.

Similarly, for a Singaporean investor whose home currency is SGD and whose stocks are bought through an investment fund denominated in SGD (non-hedged), if the underlying assets (stocks) are valued in USD, the currency risk will exist. You could buy through a fund denominated in Swiss francs, euros, pounds, or yen, it won’t affect the currency risk. This is born from the variation between the base asset (US stocks) being different to the reference or home currency (SGD).

Is Currency Hedging Useful?

Currency hedging can be useful for reducing financial uncertainty and protecting against losses caused by exchange rate fluctuations. It acts like an insurance policy, ensuring that the value of foreign investments or business transactions remain stable regardless of how the local currency moves.

Currency hedging acts as a shield against an adverse currency movement that could otherwise erode investment gains. Hedging allows for more accurate budgeting and financial planning by locking in exchange rates for future transactions. A currency may be pegged. For example, knowing the UAE Dirham is tied to the dollar gives confidence that a liability deriving from a property in the UAE is only subject to market movements in the dollar.

Hedging options can include derivative contracts such as currency options, ETFs, or companies matching revenues and expenses in the same currency. Hedging naturally comes at a cost; there are transaction and management fees, and are influenced by interest rate differentials between countries.

In equity funds, currency risk comes from the currencies of the underlying stocks the fund owns—not only the currency in which the fund itself is denominated. In contrast, the currencies used for the cash and bond portions of your portfolio deserve closer attention. For short-term horizons, these should generally align with your reference currency (matching your liabilities).

Summary

As financial planners, a customized currency strategy usually stems from areas such as scenario and retirement planning. There is no one-size-fits-all as is often the case; no one currency suits all our needs. Whether it is scenario planning, estate planning, or time horizons, all can be impacted through currency exposure. The currencies our wealth is denominated in can have significant impact upon our futures and the futures of generations to come.

Sources:

https://www.globalbankingandfinance.com/dollar-surges-us-iran-war-pushes-oil-past-100-barrel/

This material is intended for educational and informational purposes only. It is not intended to provide specific advice or recommendations for any individual. Additionally, you should consult with your Financial Advisor, Tax Advisor, or Attorney on your specific situation. The views expressed in the material are that of the author and do not necessarily reflect those of any market, regulatory body, State or Federal Agency, or Association. All efforts have been made to report or share true and accurate information. However, the information may become materially outdated or otherwise rendered incorrect due to subsequent new research or other changes, without notice. The author nor the firm are able to always verify the content from third-party sources. For additional information about the firm, please visit the MAS Website at https://www.mas.gov.sg/ and the SEC Website at www.adviserinfo.sec.gov. For a copy of the firm's ADV Part 2 Brochure, please contact us at info@avriowealth.com.